If you would like to shelter income from your crop inventory sales, starting a defined benefit retirement plan offers significant tax deductions that are much higher than SEP/Profit Sharing and 401(k) plans. These higher retirement plan deductions reduce your tax liability without borrowing and investing in more machinery.

How Does It Work

The main goal of a Defined Benefit plan is to provide a predetermined annual income benefit upon retirement. The benefit amount is determined by either the percentage of your income you would like to receive after retirement or the amount of income you choose to contribute toward the plan. To ensure the plan can pay out the intended benefit, ongoing contributions are required, accumulating sufficient retirement savings over time.

Contributions

The amount you contribute to the plan each year depends on several factors: your current age, your compensation, and the age at which you plan to retire. Generally, the older you are when you start the plan, the higher your annual contribution must be, since you have fewer years remaining to reach your savings target. Your compensation is calculated based on your business entity type, and your chosen retirement age must be at least five years after the plan is established.

Investment Strategy

The balance in your Defined Benefit plan grows as a result from your annual contributions and the performance of the investments selected within the plan. These investments can include a variety of securities, such as stocks, bonds, mutual funds, and exchange-traded funds (ETFs). Typically, a more conservative approach to asset allocation is advised to maintain both stability and growth in the plan's value. In pursuit of investment flexibility and lower fees, we do not recommend insurance products like life insurance and annuities.

Tax Implications

Establishing a Defined Benefit retirement plan offers notable tax advantages. Contributions you make are tax-deductible, which helps reduce your taxable income and, in turn, your overall tax liability. Additionally, any earnings generated by investments within the plan are tax-deferred until you begin making withdrawals in retirement. This means you do not pay taxes on investment gains each year, allowing your nest egg to grow more efficiently. However, it is important to remember that withdrawals taken during retirement will be taxed as ordinary income.

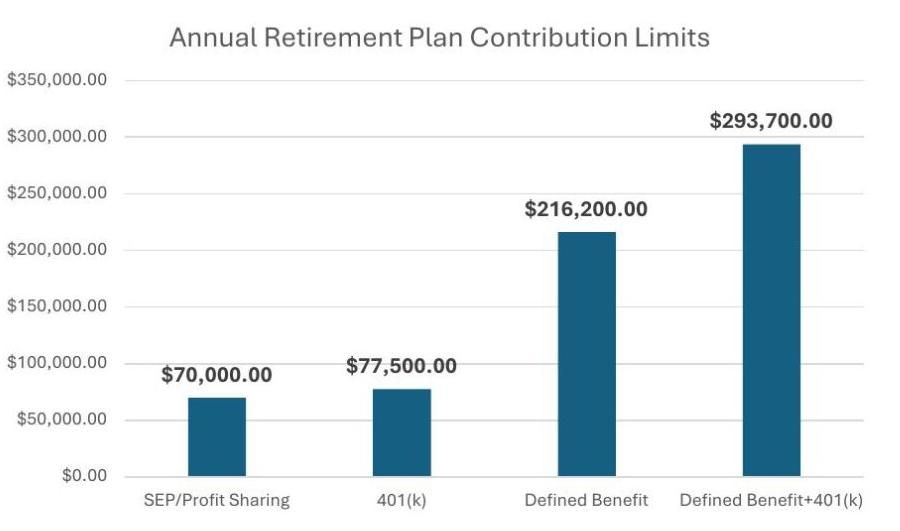

The following chart illustrates the maximum contribution limits for different retirement plans. If you are not combining a Defined Benefit plan with a 401(k) plan, you’re missing out on the tax deferred growth of larger annual contributions and substantially higher tax deductions. At the top federal tax rate, these deductions exceed $100,000!

Get Your Illustration

If you would like to see an illustration tailored to your specific situation, please call us at (319) 350-5228, contact us through our website at WWW.BRIDGEWAYWM.COM or email us at CONTACT@BRIDGEWAYWM.COM. Our team is ready to assist you with personalized guidance and examples.

Bridgeway Wealth Management LLC (BWM) is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where BWM and its representatives are properly licensed. This Article is for informational and educational purposes only. This is not an offer or solicitation for an investment. No guarantee of future results.